Remortgage Calculator

Thinking of remortgaging? Our remortgage calculator shows you what your monthly repayments could be, your potential loan-to-value and how much you could save.

Your new monthly repayment:

£

That's £ every month and £ per year.

Your new loan to value (LTV):

%

Next Steps

Speak to a broker

Ready to turn estimates into possibilities? Speak to one of our expert mortgage brokers today.

Get Started Now

How It Works

Three steps to make your mortgage possible - with expert guidance and an innovative process designed to support you every step of the way.

Get Started NowTell Us About You

Fill out a quick 60-second form about your unique situation. It won’t affect your credit score.

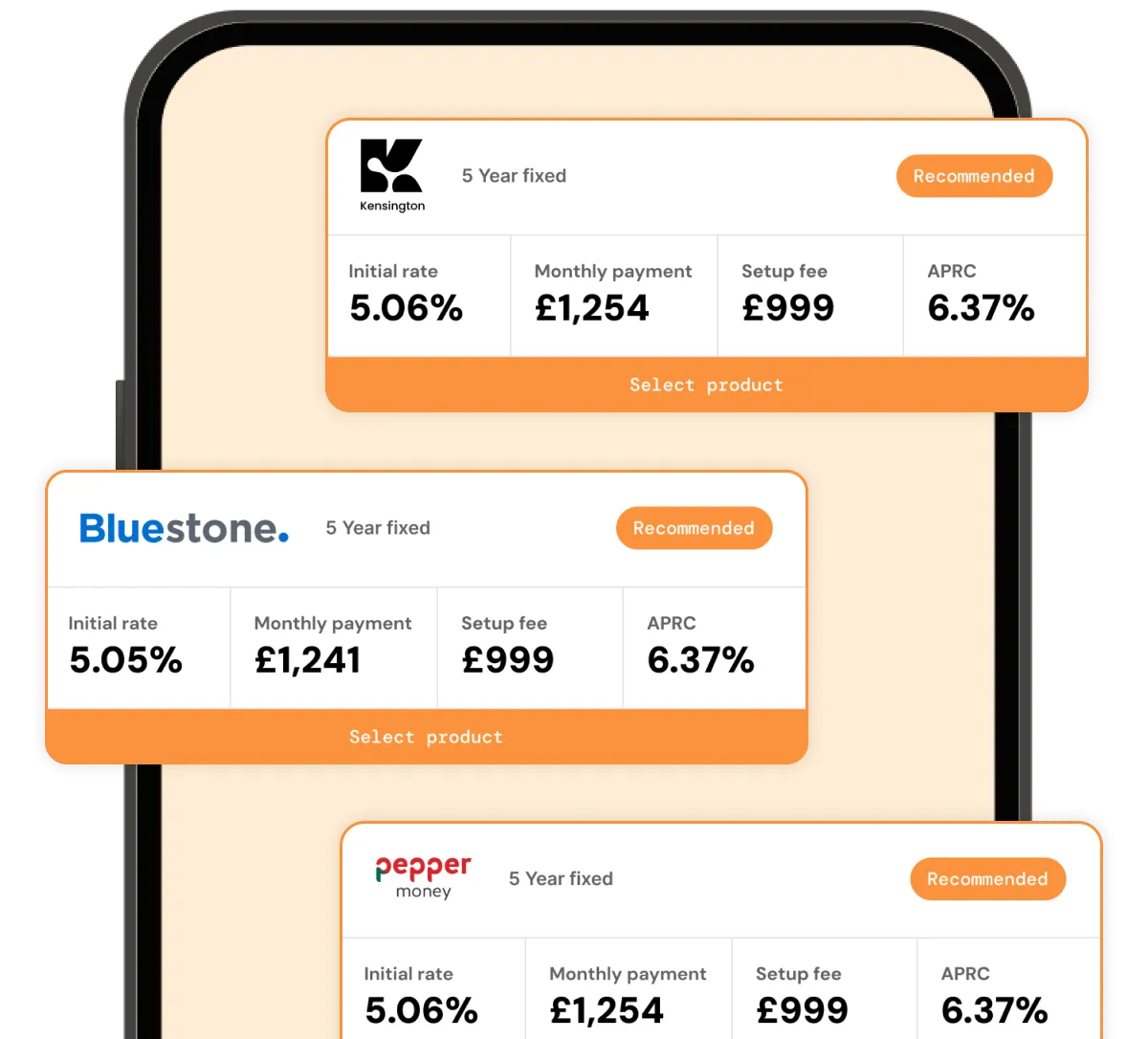

Mortgage Match

We have access to over 100 lenders, including options only available through specialist brokers, to find the best fit for you.

Meet Your Experts

Get paired with your dedicated team who'll handle everything from start to finish. Track progress 24/7 in your customer portal - no messy paperwork!

Any questions?

We're a judgement-free zone. If you still have questions, we've heard most of them before. Here are some of them answered by our team of experts.

It’s recommended to start thinking seriously about your remortgage options around 3-6 months before your current deal is due to expire. This gives you plenty of time to look at what deals are currently available and decide what options may suit you best.

Make an enquiry, and one of our Mortgage Experts can talk to you about your options in more detail. They’ll also be able to scour the market on your behalf, saving you a lot of time and, potentially, some money.

This really depends on the amount of equity you have in your property at the time. If there’s plenty you could consider releasing some of that equity for home improvements or to consolidate any other debts you may have.

A mortgage lender will calculate your loan-to-value and then consider how much additional equity can be released from your home. This will involve fresh affordability checks to ensure you can comfortably pay the new mortgage repayments.

You should be able to qualify for the best remortgage rates with a clear credit history, a healthy amount of equity in your property and a strong employment record.

A mortgage broker (like us!) will also be able to help. An experienced broker will know of specific deals not readily available on the high street or online.

Make an enquiry and one of our Mortgage Experts can talk you through some of the best remortgage deals available. This will save you a lot of time and, potentially, some money too.

Information

Tools & Guides

Haysto, a trading style of Haysto Ltd, is an appointed representative of HL Partnership Limited, which is authorised and regulated by the Financial Conduct Authority.Registered Office: Haysto, Crystal House, 24 Cattle Market Street, Norwich, NR1 3DY. Registered in England and Wales No. 12527065

There may be a fee for mortgage advice. The exact amount depends upon your circumstances, but will range from £649 to £1699, and this will be discussed and agreed with you at the earliest opportunity.

The guidance and/or information contained within this website is subject to the UK regulatory regime and is therefore targeted at consumers based in the UK.

Your home may be repossessed if you do not keep up repayments on your mortgage.